Getting coverage through a California FAIR Plan can insure your property when traditional insurance companies won’t give you a wildfire insurance policy. Here is information to help you understand what the California FAIR Plan is, what’s involved in the coverage, what it costs and whether there are any alternatives.

Table of Contents:

- Covering your house against fire in California

- What is the California FAIR Plan?

- California FAIR Plan Cost

- FAIR Plan homeowner eligibility

- What does the California FAIR Plan cover?

- What’s not covered by the California FAIR Plan?

- Issues with the California FAIR Plan and fire protection

- Is there an alternative to California FAIR Plan insurance?

- FAQs

The struggle of insuring your house against fire in California

Insurance companies are canceling coverage or not accepting new policy applications for many areas in California. When insurance is available, premiums are skyrocketing.

Insurance companies are a business operating for profit. The amount insurance companies take in as premiums and investment profits has to be greater than the amount they pay out to cover customer losses and to operate the business. Insurance companies in California are having a hard time making the math work.

On the one hand, more people living in high risk areas means insurance companies are seeing applications for more high risk properties. To cover those risks, premiums are on the rise.

At the same time, an increase in wildfires that are damaging homes is leading to more claims by customers and higher losses for insurance companies. These losses are partly due to climate change or California’s notoriously variable climate, partly due to poor fire risk mitigation processes at the national, state and local levels, and partly due to population growth and building in high burn risk areas. Again the upward pressure on insurance premiums is growing. Unaffordable premiums put insurance out of reach for many customers, even when technically still available.

While costs and losses for insurance companies are up, they are limited in their ability to raise premiums by regulation and delays by regulators in approving premium increases. It takes months to get rate increases, leaving insurers “behind the cost curve” when they do get approvals. Politicians don’t like to see rate increases, as they hurt voters’ budgets, yet they now face insurance companies pulling out of the market.

The math isn’t working for either insurance companies or their customers, making fire insurance in California tougher than ever to buy. A CA Fair Plan may be the only option for a growing number of property owners.

What is the California FAIR Plan?

The California FAIR Plan is last-resort insurance coverage for wildfires provided by a property insurance pool run by the California FAIR Plan Association. Though created by the California legislature in 1968, it is not a state agency or public entity. Instead, it is a collaboration among all property and casualty insurers licensed in the state. They work with each other, the California Department of Insurance (CDI), the legislature, and other stakeholders to share the risk for homeowners who can’t get insurance anywhere else.

How much is California FAIR Plan insurance?

California FAIR Plan insurance rates are based on negotiations with state regulators and factor in the location of your structure, its age, condition, and construction material, as well as distance to a fire station, your claims history, the types of coverage you need, and your deductible. In general, the rate you will pay will be higher than average. According to Phil Irwin, public relations representative for the California FAIR Plan, customers pay on average premiums at around $3,200.

California FAIR Plan homeowner eligibility

A California FAIR Plan is not right for everyone. To qualify, you’ll have to address several criteria:

- Property must be in California

- You must occupy the structure at least 50% of the time

- In multifamily properties you must occupy at least one of up to four units

- No claims or pre existing damage to the structure must exist

- Structure must comply with building codes

- Prove denial of coverage by at least two insurance companies

- Policies are only available through licensed agents

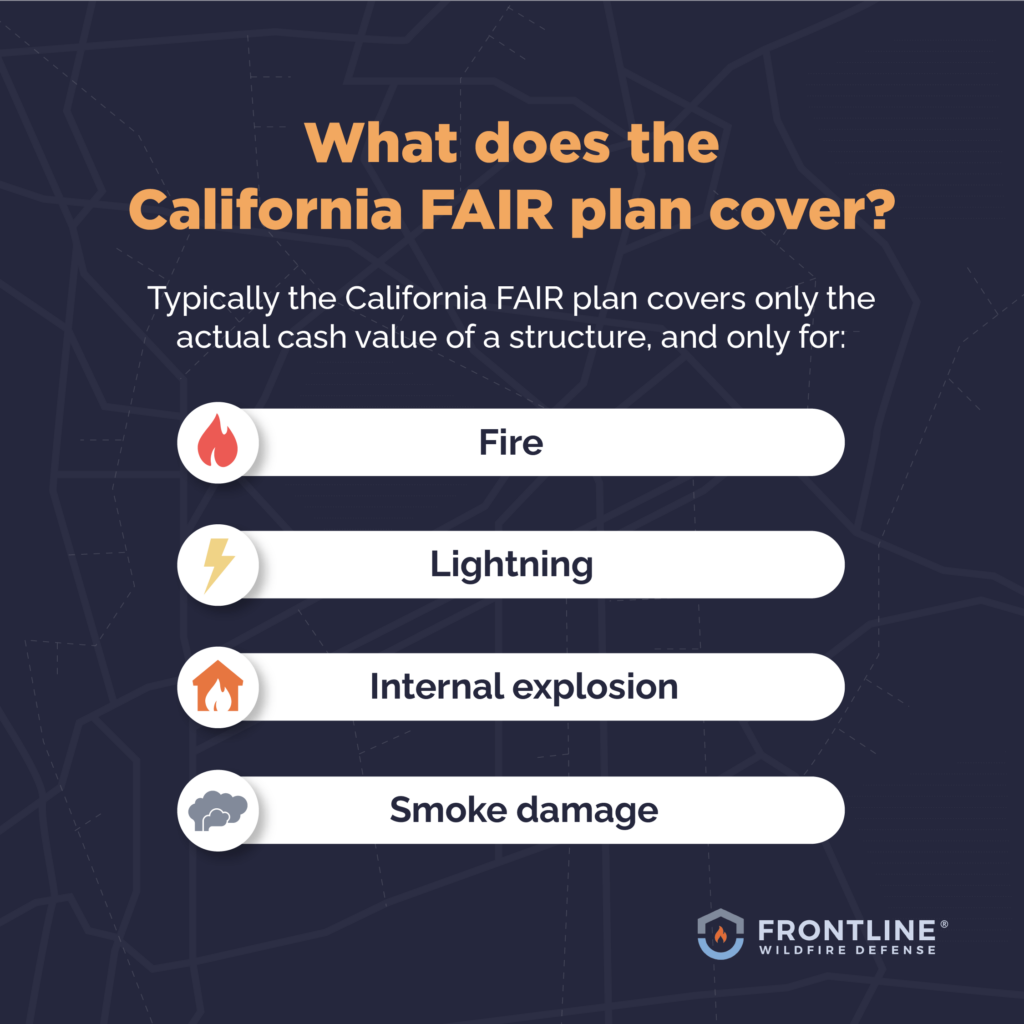

What does the California FAIR plan cover?

Typically the California FAIR plan covers only the actual cash value of a structure, and only for fire, lightning, internal explosion, and smoke damage.

You can add optional coverage for an additional cost including:

- Structure replacement to cover the cost of rebuilding, less depreciation

- Other structures such as sheds, barns, garages, fences, and porches

- Personal property coverage to replace lost belongings

- Wildfire debris removal including removal of damaged structures and remains of destroyed buildings and plants

- Landscaping to pay for restoring outdoor areas

- Flood insurance to cover damage caused by water

- Earthquake insurance to cover losses due to tectonic events

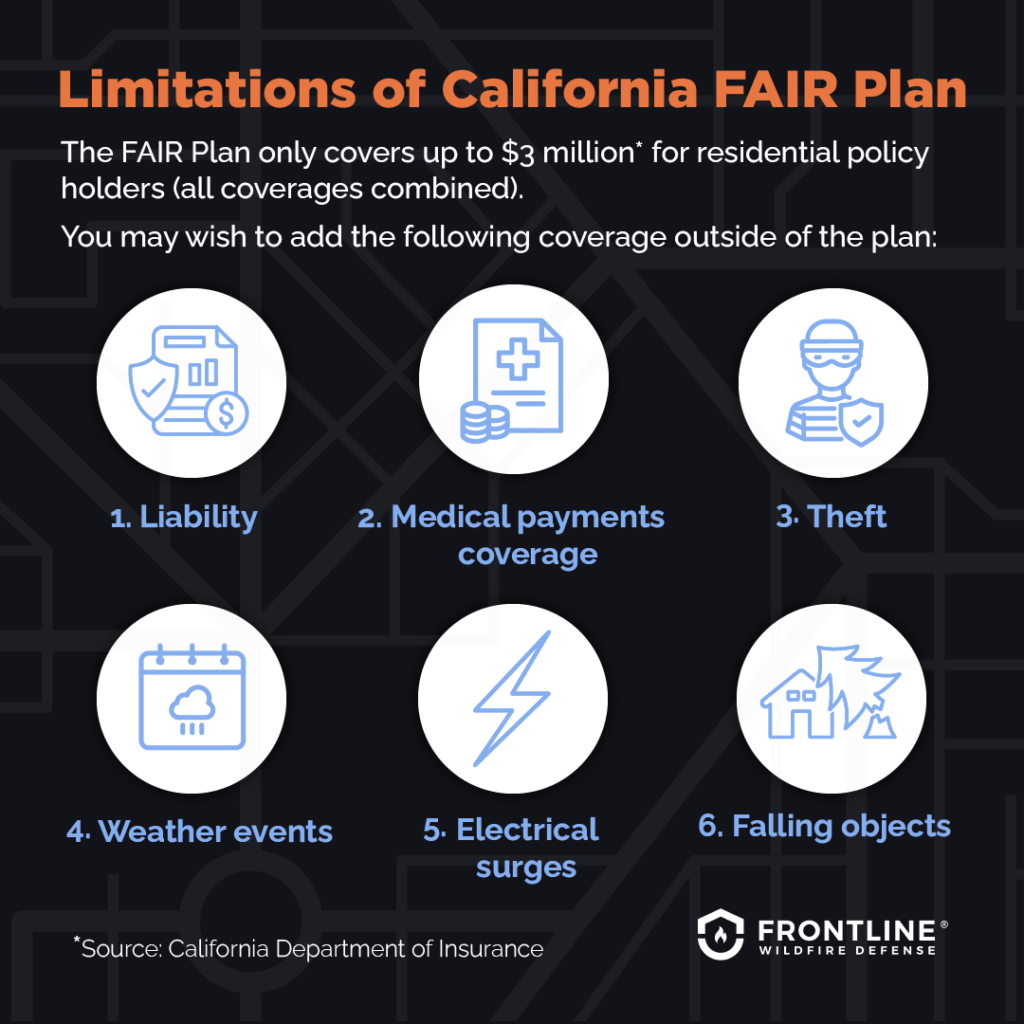

What are the limitations of California FAIR Plan insurance?

The FAIR Plan only covers up to $3 million for residential policyholders (all coverages combined) which can be a problem if you own a more expensive property.

You may wish to add the following coverage outside of the plan:

- Liability. Without this addition, you have no coverage for losses caused by you. If a guest falls in your home due to a broken step, you need liability coverage.

- Medical payments coverage. You may want coverage for injuries sustained in that fire.

- Theft or vandalism. Buy this separate coverage to protect yourself against crimes.

- Weather events. Aside from lightning, damage caused by ice, snow, freezing, wind and other weather is not covered if you don’t add this coverage..

- Electrical surges. While surges caused by a lightning strike are covered, surges coming through grid malfunctions are not included in the basic plan.

- Falling objects. The damage caused by a tree falling on your house is not included.

Issues with the California FAIR Plan and fire protection

Despite its cost and limitations, a California FAIR Plan policy is better than nothing–if you can get one. Besides meeting the stringent eligibility requirements, getting a policy has become difficult. The number of California FAIR Plans is rising fast. In 2018, FAIR wrote 126,709 policies. By 2022, the number had more than doubled to 272,826. The organization is dealing with an overload of 4,500 applications a day. It is taking months and longer for homeowners to get a response when applying. If your policy lapses and you have a mortgage, you could face high penalties from your lender every month.

Is there an alternative to California FAIR Plan insurance?

A California FAIR Plan is often the insurer of last resort. If you fail to qualify, you have no good alternatives. That does not mean you have to face wildfires with no protection at all. Homeowners are turning to wildfire defense systems to protect their property. Instead of insurance paying for your loss, these systems work to protect your house from fire altogether. If your structure can survive a wildfire with no or minimal damage, you may be better off than sifting through the wreckage and waiting for an insurance check. Prevention with a system like a wildfire roof sprinkler, can make all the difference.

FAQs

Who created the California FAIR Plan and why?

The California legislature created the California FAIR Plan by amending the California Insurance Code sections starting with 10091 in August, 1968. Wildfires and riots had created a property and casualty insurance crisis in the state, opening up a need for an insurer of last resort.

Is California FAIR Plan insurance mandatory?

While insuring your home is not mandatory, if you have a mortgage your lender may require it. Going without insurance or any protection for your property at all is risky. The California FAIR Plan is a good alternative, if you are eligible. It is not required to provide you with a policy. Despite applying and doing all you can, you may end up with no coverage.

More from the Frontline Blog

All Posts

As a Certified Partner Installer, Montana Wildfire Sprinkler Systems is the team on the ground that turns plans into...

As a Certified Partner Installer, Self Made Construction is the team on the ground that turns precision plans into...

When most people think about wildfire risk, they picture dense forests, heavy fuels, and flames moving through tree canopies....